Insurance Formulary Tiers Explained: What Tier 1, 2, 3, and Non-Formulary Mean for Your Wallet

May, 2 2026

May, 2 2026

Have you ever walked into a pharmacy, handed over your prescription, and been hit with a bill that looks nothing like what you expected? You’re not alone. The culprit is often the insurance formulary, which is a list of prescription drugs covered by your health plan, organized into cost-sharing tiers. It’s the hidden rulebook that decides whether your medication costs $5 or $150. Understanding these tiers isn’t just about saving money; it’s about knowing your rights and avoiding surprise bills that can derail your budget.

Most people assume their insurance covers all prescriptions equally. That assumption is dangerous. Insurance plans use a system called tiered formularies to manage costs. This system groups drugs based on price, brand status, and negotiated deals between insurers and drug manufacturers. If you don’t know which tier your medication falls into, you might end up paying significantly more than necessary. Let’s break down exactly how this works so you can take control of your healthcare spending.

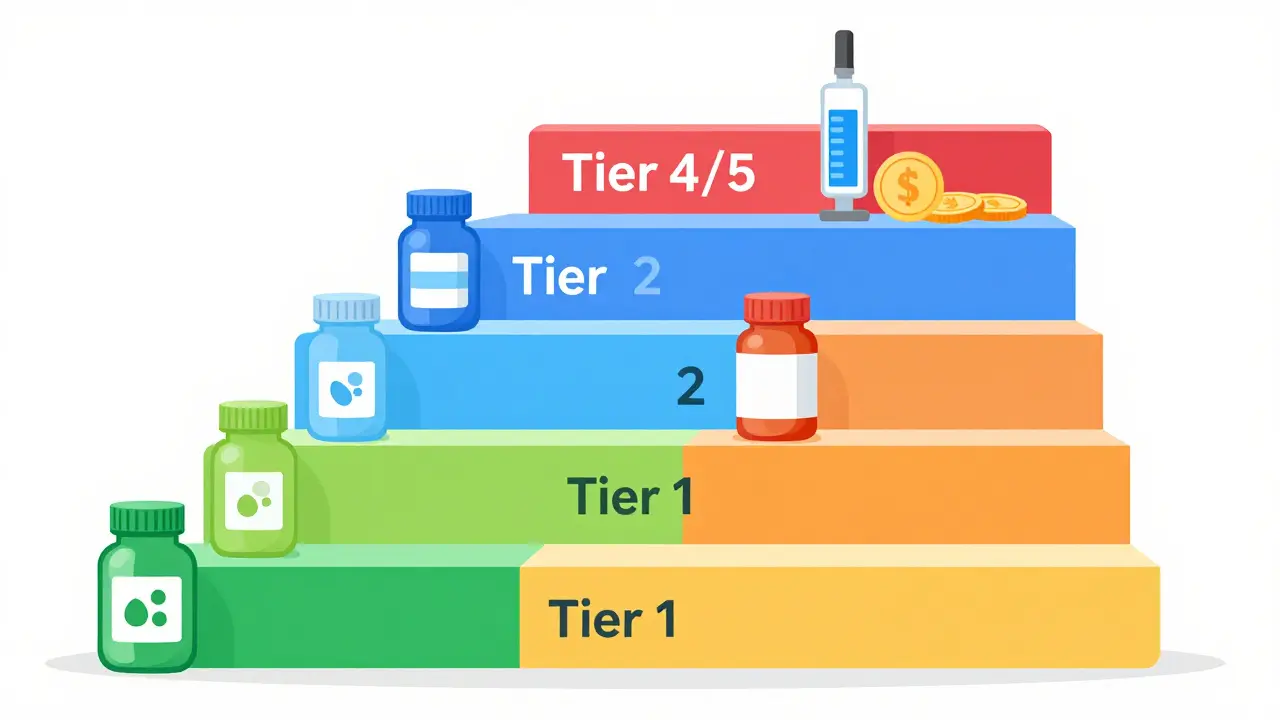

The Basics: How Formulary Tiers Work

A formulary is essentially a menu of approved medications. Insurance companies work with Pharmacy Benefit Managers (PBMs)-companies like Express Scripts, OptumRx, and CVS Caremark-to decide which drugs go on that menu and at what cost. PBMs negotiate rebates with pharmaceutical companies. In exchange for placing a drug in a lower, cheaper tier, the manufacturer pays the PBM a rebate. This system drives competition but also adds layers of complexity for patients.

The goal of tiering is simple: encourage you to choose the most cost-effective option while still providing access to necessary treatments. When you fill a prescription, the pharmacy checks your specific plan’s formulary. The tier assigned to that drug determines your out-of-pocket expense. These tiers aren’t static; they can change quarterly. As of 2023, nearly every commercial health plan and all Medicare Part D plans use this structure. Knowing your tier means knowing your true cost before you even leave the doctor’s office.

Tier 1: The Gold Standard for Savings

Tier 1 is where you want your medications to be. This tier contains preferred generic drugs and some low-cost brand-name medications. These are the drugs that have lost their patents, allowing other manufacturers to produce identical copies at a fraction of the original cost. Because they are cheap to buy, insurers place them in the lowest cost-sharing category.

- Cost: Typically $0 to $15 per prescription in commercial plans.

- Contents: Common generics for high blood pressure, cholesterol, diabetes, and basic antibiotics.

- Medicare Context: Defined as "lowest copayment" for most generic drugs.

If your doctor prescribes a Tier 1 drug, you pay almost nothing. This is the sweet spot for both patients and insurers. For example, if you need metformin for diabetes, the generic version is almost always Tier 1. Always ask your doctor if a generic alternative exists. If one does, request it specifically. This small step can save you hundreds of dollars a year without compromising your health.

Tier 2: Preferred Brand Names and Non-Preferred Generics

Tier 2 sits in the middle. It usually includes preferred brand-name drugs and some generic medications that aren’t quite as cheap or widely available as Tier 1 options. Why would a generic be Tier 2? Sometimes, a specific generic manufacturer has a better deal with the PBM, pushing another generic into Tier 2. Or, the brand-name drug might offer slight clinical advantages that justify its higher placement.

- Cost: Average copays range from $20 to $40 in commercial plans.

- Contents: Popular brand-name drugs with strong market presence, plus less common generics.

- Medicare Context: Described as "medium copayment" for preferred brand-name drugs.

This tier is where negotiation happens. If a Tier 1 generic doesn’t work for you due to side effects or allergies, your doctor might switch you to a Tier 2 brand. You’ll pay more, but it’s still manageable. Check your plan’s formulary online before filling a Tier 2 prescription. Sometimes, a different brand within the same class is Tier 1. Ask your pharmacist if there’s a therapeutic equivalent that costs less.

Tier 3: Non-Preferred Brands and Higher Costs

Tier 3 is where costs start to bite. This tier holds non-preferred brand-name drugs. These are medications where the manufacturer hasn’t offered enough rebates to secure a lower tier spot, or where no generic alternative exists yet. You might also find specialty generics here if they require special handling or storage.

- Cost: Copays typically range from $50 to $100, sometimes higher.

- Contents: Brand-name drugs without significant discounts, certain biologics, and newer medications.

- Medicare Context: Designated as "higher copayment" for non-preferred brand-name drugs.

If your medication is Tier 3, you have leverage. Don’t just pay the bill. Talk to your doctor. Is there a Tier 1 or 2 alternative that works just as well? If not, you may qualify for a formulary exception. This is a formal request to cover your drug at a lower tier cost because of medical necessity. Doctors submit clinical notes explaining why the cheaper options failed. Many patients succeed in getting their Tier 3 drugs downgraded to Tier 2 costs through this process.

Tier 4 and 5: Specialty Medications

Some plans, especially those covering complex conditions, add Tier 4 and Tier 5. These tiers are reserved for specialty medications. These aren’t your typical pills from a shelf. They are often injectable, require refrigeration, or must be administered under supervision. Think of drugs for rheumatoid arthritis, multiple sclerosis, or certain cancers.

- Cost: Usually calculated as coinsurance (a percentage of the drug’s cost), ranging from 25% to 50%.

- Contents: High-cost biologics, infusion therapies, and rare disease treatments.

- Risk: A single month’s supply can cost thousands of dollars.

The shift from fixed copays to coinsurance in these tiers is critical. If a drug costs $10,000 and your coinsurance is 30%, you pay $3,000. This creates massive financial barriers. In 2022, 41% of patients reported delaying treatment due to these high costs. If you’re facing a Tier 4 or 5 drug, immediately contact your insurer’s member services. Ask about patient assistance programs offered by the manufacturer. Most major pharma companies have foundations that help eligible patients pay for these expensive treatments. Never ignore this step.

Non-Formulary Drugs: The Coverage Gap

What if your drug isn’t on the list at all? That’s a non-formulary drug. Technically, your insurance doesn’t cover it. You could be responsible for 100% of the cost. However, "non-covered" doesn’t always mean "no coverage." Insurers are required to allow appeals. If a doctor proves that no formulary alternative is medically appropriate, they can request coverage for the non-formulary drug.

This process is slower and more difficult than standard tier exceptions. It requires extensive documentation. Be prepared to fight for this coverage. Use resources like the Patient Advocate Foundation, which offers free case management for patients navigating these issues. Don’t accept "it’s not covered" as a final answer without exploring the appeal process first.

| Tier | Typical Contents | Estimated Cost (Commercial) | Best Strategy |

|---|---|---|---|

| Tier 1 | Preferred Generics | $0 - $15 | Always choose generic if available |

| Tier 2 | Preferred Brands / Some Generics | $20 - $40 | Check for therapeutic equivalents |

| Tier 3 | Non-Preferred Brands | $50 - $100+ | Request formulary exception |

| Tier 4/5 | Specialty/Biologics | 25% - 50% Coinsurance | Seek manufacturer assistance programs |

| Non-Formulary | Not Listed | 100% Patient Responsibility | Fight for coverage via appeal |

Why Do Tiers Change?

You might notice your drug moves from Tier 2 to Tier 3 overnight. This happens because formularies are dynamic. PBMs constantly renegotiate contracts. If a manufacturer stops offering rebates, their drug gets bumped to a higher tier. New generics entering the market can push older brands up. Regulatory changes, like the Inflation Reduction Act capping insulin costs, also force adjustments. These changes can occur quarterly, meaning your costs can shift four times a year. Stay vigilant. Review your plan’s Summary of Benefits and Coverage (SBC) during open enrollment and whenever you receive a new formulary update.

How to Navigate Your Formulary Like a Pro

Understanding the tiers is only half the battle. You need actionable steps to manage your costs. First, never rely solely on the sticker price at the pharmacy counter. Use your insurer’s online tool or app to check the exact tier and cost before you fill the prescription. Second, build a relationship with your pharmacist. They see formulary trends daily and can often suggest cheaper alternatives that your doctor might not know about. Third, keep records of any formulary exceptions or appeals. If a denial happens, having a paper trail makes overturning it easier.

If you’re on Medicare, remember the 2024 redesign of Part D. The new catastrophic phase reduces out-of-pocket costs for high-tier drugs significantly. If you’re in a commercial plan, look for value-based tiering, where drugs that improve long-term outcomes get lower costs. This is becoming more common. Finally, don’t hesitate to call your insurer. Their customer service reps can explain why a specific drug is placed in a certain tier and guide you through the exception process. Knowledge is your best defense against unexpected medical bills.

Can I switch my insurance plan mid-year if my drug becomes too expensive?

Generally, no. You can only change plans during Open Enrollment unless you experience a Qualifying Life Event, such as losing job-based coverage, moving to a new area, or getting married. If your drug costs spike due to a tier change, your best immediate option is to request a formulary exception or seek a manufacturer assistance program rather than switching plans.

What is the difference between a copay and coinsurance?

A copay is a fixed amount you pay for each prescription, such as $20. It stays the same regardless of the drug's actual price. Coinsurance is a percentage of the drug's cost, such as 20%. If the drug costs $500, you pay $100. Coinsurance is common in Tier 4 and 5 specialty drugs and can lead to much higher out-of-pocket expenses.

How do I apply for a formulary exception?

Your prescribing physician must submit a request to your insurance company or PBM. They need to provide clinical evidence showing that all formulary alternatives have failed or are contraindicated for your condition. This process usually takes 7 to 14 business days. You can expedite it if your health is at risk by requesting an urgent review.

Why is my generic drug in Tier 2 instead of Tier 1?

Not all generics are created equal in the eyes of PBMs. Some generic manufacturers have better rebate agreements with the PBM than others. Additionally, some generics may have bioavailability issues or require special handling, placing them in a higher tier. Ask your pharmacist if another generic manufacturer of the same drug is available at a lower tier.

Are formulary tiers the same for everyone?

No. Tiers vary by insurance plan, employer group, and even individual state regulations. Two people with the same brand of insurance might have different tier assignments for the same drug depending on their specific plan design. Always check your own plan’s formulary document rather than relying on general information.

Jimmy Crocker

May 3, 2026 AT 22:28It is truly disheartening to observe the sheer lack of intellectual rigor displayed by the general populace when confronted with the rudimentary mechanics of pharmaceutical economics, which are, in fact, quite elegant in their predatory simplicity. One might assume that a basic understanding of supply and demand would suffice for any educated individual, yet here we are, wading through a swamp of confusion regarding these so-called 'tiers,' as if they were some arcane mystery rather than a straightforward mechanism of cost-shifting designed by individuals who likely hold advanced degrees in finance or law. The article, while adequate for those whose cognitive faculties have been dulled by years of consuming processed media, fails to adequately address the deeper structural issues inherent in the PBM model, which is essentially a middleman racket that has grown fat on the backs of the sick and the ignorant. I find it amusing that people think checking an app is sufficient due diligence, when in reality one must understand the rebate structures and the opaque negotiations that occur behind closed doors between executives who probably do not even know what a formulary is beyond its impact on their quarterly bonuses. It is a shame that education has declined to such a level that this information needs to be spoon-fed in bullet points, but perhaps that is simply the nature of our current societal trajectory towards mediocrity.

Joel Bonstell

May 5, 2026 AT 04:37Hey everyone! Just wanted to chime in because i totally get how confusing this stuff can be. I used to work at a pharmacy for a few years and honestly seeing ppl get hit with huge bills was heartbreaking. If you're on a tier 3 drug, dont just pay it! Ask your doc for a prior auth or exception. It saves so much hassle later. Also, generics are usually great unless you have a specific sensitivity. Hope this helps someone out there!

Andrew Hanssen

May 6, 2026 AT 07:52The entire premise of this discussion is flawed because it accepts the legitimacy of a system that is fundamentally broken and exploitative. You are all dancing to the tune of corporate greed without realizing that the 'savings' offered by Tier 1 are merely crumbs from the table of a banquet you cannot afford. The real issue is not which tier you fall into, but why you need permission from a faceless bureaucracy to access medication that should be a basic human right. This tiered structure is nothing more than a sophisticated method of rationing healthcare based on wealth rather than medical necessity, and pretending otherwise is an act of self-deception. We should not be discussing how to navigate this maze; we should be demanding its complete demolition.

Prudence Wesson

May 7, 2026 AT 10:32Oh, please!! Do you really think reading this fluff will solve your problems?? It's obvious you've never actually dealt with a real insurance claim denial!! They lie!! They always lie!! And don't get me started on the PBMs!! They are evil!! You need to fight harder!! Don't let them push you around!! It's not about tiers!! It's about power!!

Alexa Mack

May 8, 2026 AT 10:16I found this really helpful, thanks for sharing! I was confused about why my generic was suddenly more expensive. Turns out it was a different manufacturer. My pharmacist helped me switch back to the cheaper one. It's crazy how much money adds up. I think we need more transparency in this whole system. Has anyone else had success with formulary exceptions? I'm thinking about trying it for my mom's meds.

Divya Patel

May 8, 2026 AT 21:35One must consider the philosophical implications of commodifying health; when life-saving drugs are placed on a menu like items in a restaurant, we lose sight of the intrinsic value of human well-being. In India, we often struggle with similar issues, though the dynamics are different. The concept of 'tiers' creates a hierarchy of care that mirrors societal inequalities. It is important to remember that knowledge is power, but empathy is wisdom. Let us use this information not just to save money, but to advocate for a more equitable system where no one is left behind due to arbitrary bureaucratic classifications.

SWATI NAWANGE

May 10, 2026 AT 02:14This is absolutely ridiculous!! How dare you suggest that we should just accept these costs!! It is an insult to our intelligence!! I am paying thousands for my specialty drugs and the insurance company laughs in my face!! They don't care about us!! They only care about their profits!! This is why the system is failing!! We need change NOW!! Not more articles!! Action!!

nikki paurillo

May 10, 2026 AT 10:38It’s like walking through a minefield, isn’t it? One step wrong and boom-your wallet is blown to smithereens. I love how the article breaks it down, but honestly, it feels like learning a new language just to buy a pill. I had a friend who spent weeks fighting for a formulary exception, and she finally got it, but the stress was enough to give her heart palpitations. We need to stop treating healthcare like a shopping spree and start treating it like a right. Until then, we’re all just bargaining chips in a game we didn’t agree to play.

Tallulah Sandison

May 10, 2026 AT 17:38Great info! I learned something new today. Thanks for posting this. Keep up the good work!

Ken Baldridge

May 11, 2026 AT 07:28Folks, let's break this down with some strategic insight. The key takeaway here is leverage. When you engage with your PBM, you are entering a negotiation paradigm. Utilize the clinical data points provided by your physician to create a robust case for formulary exceptions. Remember, the goal is to optimize your therapeutic outcomes while minimizing financial exposure. It's all about aligning your stakeholder interests with the insurer's risk management protocols. Stay proactive, stay informed, and don't let the bureaucratic inertia dictate your health journey.

Bradley Gusick

May 12, 2026 AT 02:33This is exactly what happens when you let globalists run your healthcare system. They want to control every aspect of your life, including what goes into your body. The tiers are just a way to segregate the population and make sure only the elite get the best treatments. Wake up, sheeple! The government and the big pharma companies are working together to enslave us. Don't trust them. Stock up on supplies and prepare for the collapse.

Leah Sentz

May 13, 2026 AT 22:09Ugh!! Why is this so complicated?? 😡😡 I hate insurance companies!! They are all scammers!! 🤬🤬 I paid $500 for a prescription last month and it was supposed to be covered!! Unbelievable!! 😤😤 We need to boycott them all!! #HealthcareScam #Angry 😠😠